We're branching beyond SEO content here because startup readers ask us about the full GTM stack, and corporate cards are foundational — they touch every team's spend, every SaaS subscription, and every reconciliation cycle. Get this layer right and your finance team disappears into the background; get it wrong and you'll burn 5-10 hours a week on receipt chasing, manual categorization, and expense report friction that compounds with every new hire.

A couple of heavily-marketed fintech names dominate the conversation when founders search for "best corporate cards" — but plenty of strong options exist, each optimized for different stages, geographies, and workflows. The 10 cards below cover the genuine range of what's available: fintech-native platforms (Mercury, Rho, Float) that bundle banking and cards with no personal guarantee, free spend management platforms (Bill Spend & Expense), procure-to-pay systems for mid-market (Airbase), traditional bank cards with serious rewards programs (AMEX, Capital One, Chase), developer-first issuing APIs (Stripe), and travel-bundled platforms (Navan).

We evaluated each on the four things startup founders actually care about: no personal guarantee options (so your house isn't collateral for SaaS subscriptions), programmable virtual cards (so you can isolate every vendor relationship), real-time spend controls (so finance isn't the bottleneck for every $20 software purchase), and accounting integrations (so QuickBooks, Xero, or NetSuite reconciliation happens automatically). Whether you're pre-seed, Series B, or scaling past $50M ARR, there's a fit here.

Quick Comparison

| Card | Best For | Annual Fee | Rewards |

|---|---|---|---|

| Mercury | Overall for Startups | Free | 1.5%-2.5% cashback |

| Rho | Premium All-in-One | Free | 1.25% cashback |

| Bill Spend & Expense | SMB Spend Management | Free | 1x-7x points |

| Airbase | Mid-Market | Custom | Variable |

| AMEX Business Platinum | Premium Travel | $695 | 5x travel points |

| Capital One Spark Cash Plus | Traditional Cashback | $150 | 2% unlimited |

| Stripe Issuing | Developer-First | Free | Custom |

| Float | Canadian Startups | Free | 1% cashback |

| Chase Ink Preferred | Travel Rewards | $95 | 3x business categories |

| Navan Connect | Travel + Expense | Free | Travel credits |

Why Startups Need a Real Corporate Card

Founders often start by running company spend on personal cards or a single owner-name business credit card. That works for the first 3-6 months — then it doesn't. As soon as you have one employee, two SaaS subscriptions per role, and any kind of investor-facing reporting requirement, the personal-card setup becomes a tax on every reconciliation cycle. A proper corporate card platform solves four structural problems at once:

No Personal Guarantee

Fintech-native cards (Mercury, Rho, Bill, Stripe, Float) underwrite based on business cash balance or revenue — not your personal credit. Your house, your car, and your personal score stay separate from your company's spend.

Virtual Cards for SaaS Spend

Modern corporate cards let you issue unlimited virtual cards — one per SaaS subscription. Cancel a vendor? Burn the virtual card without touching your physical card. Catch shadow IT spend? Each subscription leaves a fingerprint.

Real-Time Spend Controls

Set per-card limits, merchant category restrictions, and approval workflows — enforced at the network level. Finance teams stop being the bottleneck for every employee's $50 software request and start being a strategic function.

Accounting Integrations

Real-time bidirectional sync with QuickBooks, Xero, NetSuite, or Sage Intacct. Transactions auto-categorize, receipts attach automatically, and month-end close drops from 5 days to 5 hours. The integration depth is the difference between fintech-native and traditional cards.

Pro Tip

The highest-leverage corporate card decision is usually choosing your platform before you have a finance hire. Get this layer wired correctly when you have 3 people and the eventual 30-person team inherits clean operations. Re-platforming corporate cards at scale is genuinely painful.

Rewards Rate at a Glance

Here's how the 10 cards compare on rewards rates. Fintech-native cards (green) deliver simple cashback, traditional bank cards (blue/orange) deliver points programs that need optimization, and platform cards (purple) trade rewards for advanced workflow features:

What Makes a Great Corporate Card in 2026

The corporate card category has matured dramatically in the past five years. The picks that matter today share four common features — and any card missing them in 2026 is fundamentally a step backward:

No Personal Guarantee Options

For VC-backed startups, fintech-native cards underwrite on business balance, not founder credit. Mercury, Rho, Bill, Stripe, and Float all do this for qualifying businesses. Traditional cards almost universally require a personal guarantee — a hard line many founders won't cross.

Programmable Virtual Cards

Unlimited virtual cards with API access, merchant-specific spend limits, and one-time-use options. This is table stakes in 2026 — Stripe Issuing turned it into infrastructure, and every fintech card now offers it. Traditional bank cards mostly don't.

Real-Time Spend Controls

Network-level enforcement of spend limits, merchant restrictions, and approval thresholds. Bill, Rho, and Mercury are best-in-class. The test: can you issue a card that only works at Stripe for exactly $99 once? If yes, you have real spend controls.

Accounting Integrations

Bidirectional sync with QuickBooks Online, Xero, NetSuite, or Sage Intacct. Bill Spend & Expense leads on depth (entire Bill.com infrastructure), Airbase wins on NetSuite, and Mercury/Rho deliver competitive QuickBooks integration. Traditional cards lag.

Mercury

Best for: Early-stage startups that want banking and a corporate card in one platform with no personal guarantee

Mercury is the corporate card most early-stage startups should start with — and most should stay with through Series B. The IO Card sits on top of Mercury's banking platform, so the same account you're already using for payroll, vendor payments, and Stripe payouts also issues virtual and physical cards with 1.5%-2.5% cashback. No annual fee, no personal guarantee, and the underwriting is based on your Mercury balance rather than personal credit. For VC-backed startups with funding sitting in the bank, qualifying is a non-issue. The unified banking-plus-cards experience eliminates the reconciliation headaches you get when banking and cards live in separate systems.

Key Features

- Mercury IO Card: Virtual and physical cards with 1.5%-2.5% cashback, no annual fee, no personal guarantee for qualifying businesses

- Unified Banking + Cards: Same platform handles business checking, savings, wires, ACH, and cards — single source of truth for spend

- Unlimited Virtual Cards: Spin up vendor-specific virtual cards for every SaaS subscription, with per-card spend limits

- Treasury Account: FDIC-insured up to $5M with yields on idle cash — funded automatically from your operating account

- QuickBooks + Xero Integration: Real-time transaction sync with auto-categorization, receipts attached at the transaction level

Pricing & Rewards

| Detail | Rate / Fee | Notes |

|---|---|---|

| Mercury IO Card | Free | Free |

| Cashback Rewards | 1.5%-2.5% | 1.5%-2.5% on all spend |

| Mercury Plus | $35 | $35/mo (advanced features) |

Pros

- Best banking-plus-cards integration for startups, full stop

- No personal guarantee required for qualifying VC-backed startups

- Treasury yields on idle cash genuinely move the needle on runway

- Unlimited free virtual cards make SaaS subscription management trivial

Cons

- Cashback tiers require maintaining higher Mercury balances

- Not ideal for businesses without institutional funding or significant revenue

- International transactions less polished than dedicated travel cards

Verdict: If you're a VC-backed startup early in the journey, open Mercury first. The unified banking-plus-cards platform compounds operationally, and most startups never need to add another corporate card provider.

Visit MercuryRho

Best for: Growth-stage startups needing banking, AP automation, treasury, and cards in one unified platform

Rho is what Mercury wants to be when it grows up — a full finance platform that combines business banking, corporate cards, accounts payable automation, treasury management, and expense controls in a single product. For growth-stage startups (Series A through C) that have outgrown the simplicity of Mercury but don't want to stitch together five different finance tools, Rho is the sharpest pick on the market. The card program is competitive (1.25% cashback on most spend), but the real value is the workflow consolidation: invoice approvals, vendor payments, employee reimbursements, and corporate cards all live in one platform with one source of truth.

Key Features

- Rho Corporate Card: Charge card with 1.25% cashback, unlimited virtual cards, granular spend controls

- AP Automation: Capture invoices, route through approval workflows, and pay via card, ACH, wire, or check from one platform

- Treasury Management: Automated cash sweeps into yield accounts, FDIC-insured up to $75M via partner networks

- Expense Management: Receipt capture, mileage tracking, employee reimbursements — all in the same app as cards

- ERP Integrations: Real-time sync with NetSuite, QuickBooks Online, Xero, and Sage Intacct

Pricing & Rewards

| Detail | Rate / Fee | Notes |

|---|---|---|

| Rho Platform | Free | Free (core platform) |

| Cashback Rewards | 1.25% | 1.25% on most spend |

| Treasury Yields | Variable | Market-rate yields on idle cash |

Pros

- Best workflow consolidation in startup fintech — banking, AP, cards, treasury in one platform

- Treasury management at $75M FDIC coverage materially de-risks larger cash positions

- AP automation reduces invoice processing time by 70%+ for most teams

- Strongest NetSuite integration of any fintech corporate card platform

Cons

- Less suited to early-stage startups (under $1M ARR) who don't need the full platform

- Cashback rate (1.25%) lower than Mercury's top tier

- Onboarding requires more setup than simpler card-only providers

Verdict: Rho is the right call when you've outgrown Mercury's simplicity and need real finance automation. The integrated platform pays off operationally within the first quarter for growth-stage startups.

Visit RhoBill Spend & Expense

Best for: Small and mid-sized businesses managing 10+ cardholders that need free spend controls and approval workflows

Bill Spend & Expense (formerly Divvy, acquired by Bill.com and rebranded) is the most fully-featured free corporate card platform on the market. The economics work because Bill earns interchange revenue — you get unlimited virtual cards, real-time spend controls, multi-level approval workflows, and rewards points at zero platform cost. For small and mid-sized businesses with 10+ employee cardholders that don't want to pay premium platform prices or stitch together SaaS subscriptions for expense management, Bill is genuinely category-leading. The accounting integration is also the deepest in this guide thanks to native Bill.com infrastructure.

Key Features

- Free Corporate Cards: Unlimited virtual and physical cards with no platform fee, funded via charge card model

- Real-Time Spend Controls: Set per-card budgets, merchant restrictions, and time-based limits with instant enforcement

- Approval Workflows: Multi-level approval routing for spend requests and reimbursements — configurable by team, amount, or category

- Rewards Points: Earn points on every transaction, redeemable for travel, gift cards, or statement credits

- Bill.com Accounting Integrations: Bidirectional sync with QuickBooks, Xero, NetSuite, Sage Intacct — deepest accounting integration in the category

Pricing & Rewards

| Detail | Rate / Fee | Notes |

|---|---|---|

| Platform Fee | Free | Free |

| Rewards Points | 1x-7x | Category-based points multipliers |

| Annual Card Fee | $0 | $0 per card |

Pros

- Genuinely free with full spend management feature set

- Deepest accounting integrations in the corporate card category

- Approval workflows mature enough for 50+ cardholder teams

- Points program competitive with premium paid platforms

Cons

- Charge card model means full balance due monthly (no carrying balances)

- Underwriting more conservative than Mercury for early-stage startups

- Customer support sometimes lags Mercury and Rho on response time

Verdict: If you have 10+ employees needing cards and don't want to pay platform fees, Bill Spend & Expense is the obvious pick. The combination of free + deep accounting integration + approval workflows is unmatched at this price.

Visit Bill Spend & ExpenseAirbase (Paylocity)

Best for: Mid-market companies ($25M-$500M revenue) needing enterprise-grade procure-to-pay with corporate cards bundled in

Airbase (now part of Paylocity following the 2024 acquisition) is the procure-to-pay platform mid-market finance teams use when Bill Spend & Expense isn't sophisticated enough and Coupa is overkill. The corporate card program is a component of a much larger system that handles procurement requests, vendor onboarding, invoice processing, approval workflows, and AP — all wired into NetSuite, Sage Intacct, or Microsoft Dynamics. For finance teams at companies with $25M+ revenue and 50+ employees, the procure-to-pay consolidation justifies the premium pricing. The corporate cards alone aren't the reason to buy Airbase; the unified P2P platform is.

Key Features

- Corporate Cards + Procurement: Cards integrated into the same platform as procurement requests, vendor management, and AP

- Enterprise Approval Workflows: Complex multi-stakeholder routing with custom logic — built for finance teams at companies with 100+ employees

- Advanced NetSuite Integration: Real-time, bidirectional sync with NetSuite including custom field mapping and subsidiary support

- Vendor Management: Vendor onboarding, W-9 collection, 1099 reporting, and ACH/wire/card payments from one workflow

- Audit-Ready Reporting: Compliance-grade audit trails, SOX-ready controls, and segregation of duties built-in

Pricing & Rewards

| Detail | Rate / Fee | Notes |

|---|---|---|

| Standard | Custom | Custom pricing by company size |

| Premium | Custom | Custom (includes advanced workflows) |

| Enterprise | Custom | Custom (includes SOC compliance support) |

Pros

- Strongest procure-to-pay platform with corporate cards in this guide

- NetSuite integration unmatched in the mid-market segment

- Approval workflows handle genuine enterprise complexity

- SOX-ready audit trails reduce compliance burden meaningfully

Cons

- Pricing premium versus pure card platforms — typically $40K-$150K+ annually

- Overkill for companies under $25M revenue

- Implementation timeline (8-16 weeks) longer than fintech-native alternatives

Verdict: Airbase is the right call when finance team size and procure-to-pay complexity make standalone card platforms insufficient. Most companies under $25M revenue should stay with Bill Spend & Expense or Rho.

Visit Airbase (Paylocity)American Express Business Platinum

Best for: Travel-heavy startups and founders who already maximize personal AMEX Platinum and want business-side parallel benefits

The AMEX Business Platinum is the premium points card most legitimate for startups whose teams travel heavily — particularly for founders pitching investors, conferences, or building international partnerships. 5x points on flights and prepaid hotels booked through Amex Travel, generous travel credits ($200 airline incidental, $189 CLEAR, $200 hotel collection), and Centurion Lounge access make the $695 annual fee defensible for the right profile. It's not a startup operations card — the personal guarantee, charge card structure, and points game make it ill-suited for general team spend. But for the founder/exec card line in a travel-heavy business, it's worth running parallel to a fintech card platform.

Key Features

- 5x Travel Rewards: 5 Membership Rewards points per dollar on flights and prepaid hotels through Amex Travel

- Centurion Lounge Access: Unlimited access to Centurion Lounges plus Priority Pass Select for cardholder and 2 guests

- Travel Credits Bundle: $200 airline credit, $189 CLEAR Plus credit, $200 Fine Hotels collection credit annually

- Hotel Elite Status: Marriott Bonvoy Gold and Hilton Honors Gold status as cardholder benefits

- Welcome Bonus: 150,000 Membership Rewards points after qualifying spend in the first 3 months

Pricing & Rewards

| Detail | Rate / Fee | Notes |

|---|---|---|

| Annual Fee | $695 | $695/yr |

| Travel Rewards | 5x | 5x points on flights and prepaid hotels |

| Signup Bonus | 150K | 150K points after qualifying spend |

Pros

- Best premium travel rewards for businesses, when redemption is optimized

- Centurion Lounge access genuinely valuable for founders flying 20+ times annually

- Membership Rewards points have multiple high-value transfer partners

- Strong purchase protection and travel insurance benefits

Cons

- $695 annual fee requires deliberate optimization to justify

- Personal guarantee required — your credit is on the hook

- Charge card structure means full balance due monthly

- Maximizing benefits requires time investment most founders won't make

Verdict: AMEX Business Platinum makes sense as the founder/exec travel card running parallel to a fintech card platform — not as your team's general spend card. Only worth it if you'll actually use the lounge access and travel credits.

Visit American Express Business PlatinumCapital One Spark Cash Plus

Best for: Established businesses with strong personal credit wanting simple 2% cashback on all spend

Capital One Spark Cash Plus is the traditional-bank corporate card most worth considering when fintech alternatives don't fit — typically when you have established business credit, can absorb a $150 annual fee, and want flat 2% cashback with no category restrictions. It's a charge card (no carrying balance), so cash flow discipline matters, but the simplicity is the appeal: no points game, no rotating categories, no minimum balance gating, just 2% back on every dollar spent. The $150 annual fee is offset after roughly $7,500 in annual spend versus a no-fee card, which most established businesses clear in a month.

Key Features

- Unlimited 2% Cashback: Flat 2% back on every purchase, no category restrictions, no caps, no rotating bonuses

- Annual Cash Bonus: $200 cash bonus annually after spending $200K in qualifying purchases

- Free Employee Cards: Add unlimited employee cards at no additional cost, with individual spend limits

- No Foreign Transaction Fees: International purchases without the 2.7%-3% surcharge typical of business cards

- Real-Time Mobile Notifications: Instant alerts for all transactions across employee cards

Pricing & Rewards

| Detail | Rate / Fee | Notes |

|---|---|---|

| Annual Fee | $150 | $150/yr |

| Cashback | 2% | 2% unlimited on all spend |

| Foreign Transaction Fee | $0 | None |

Pros

- Simplest high-value cashback structure available — 2% flat, no thinking required

- No foreign transaction fees rare among traditional business cards

- Free unlimited employee cards with spend controls

- Capital One's mobile app and reporting are best-in-class for traditional bank cards

Cons

- Personal guarantee almost always required

- Charge card structure means no extended financing options

- Less competitive than fintech cards on spend management features

- Annual fee tax on early-stage businesses with limited spend

Verdict: Spark Cash Plus is the right call when you want simple, high-cashback rewards from a traditional bank without playing the points optimization game. Works best for established businesses, not pre-revenue startups.

Visit Capital One Spark Cash PlusStripe Issuing

Best for: Developer-led companies that want to issue programmable corporate cards via API and embed card logic into their product

Stripe Issuing is the corporate card product for companies that don't think of cards as a finance team workflow — they think of cards as a programmable primitive. Issue cards via API, control spend in real-time with webhook-driven authorization logic, generate one-time virtual cards for specific transactions, and embed everything into your existing product or internal tooling. For developer-first startups (devtools, fintech, marketplaces, SaaS with reimbursement needs), Stripe Issuing turns corporate cards into infrastructure rather than a UI you have to log into. Not the right pick if you want a polished out-of-the-box experience — but unmatched if you want full programmatic control.

Key Features

- Card Issuing API: Programmatically create virtual and physical cards with spend controls, all via REST API

- Real-Time Authorization: Webhook every authorization request and approve/decline based on your custom business logic

- Global Availability: Issue cards in 40+ countries with local currencies and regional payment networks

- Spending Controls: Set per-card limits, merchant category restrictions, and time-based rules programmatically

- Stripe Treasury Integration: Combine issued cards with Stripe Treasury accounts for a complete embedded finance stack

Pricing & Rewards

| Detail | Rate / Fee | Notes |

|---|---|---|

| Platform Fee | Free | No platform fee |

| Physical Card Fee | $3 | $3 per physical card issued |

| Interchange Revenue Share | Variable | Share of interchange on card spend |

Pros

- Most programmable corporate card product available, full stop

- Global card issuing in 40+ countries beats any fintech alternative

- Real-time authorization webhooks unlock genuinely novel use cases

- Stripe ecosystem integration (Treasury, Payments, Connect) is seamless

Cons

- Requires engineering investment to use effectively — not a turnkey product

- No out-of-the-box spend management UI for finance teams

- Reporting and reconciliation tooling thinner than dedicated card platforms

- Best for companies already on Stripe's payments stack

Verdict: Stripe Issuing is the right call for developer-first companies that want cards as infrastructure. Pair with a fintech-native card (Mercury or Rho) for your finance team's day-to-day spend.

Visit Stripe IssuingFloat

Best for: Canadian-incorporated startups that need CAD-native corporate cards with spend management and no personal guarantee

Float is the dominant corporate card platform for Canadian startups — the same playbook Mercury runs in the US, executed for the CAD-denominated market with Canadian banking integrations and no personal guarantee underwriting. Virtual and physical cards, real-time spend controls, automated receipt capture, and bidirectional sync with QuickBooks Online and Xero. For Canadian founders who'd otherwise be stuck on traditional bank cards (which require personal guarantees and offer worse spend controls), Float is a genuine category-leading alternative. US-incorporated founders with Canadian entities should run Float in parallel to their US card stack.

Key Features

- CAD-Native Corporate Cards: Virtual and physical cards in Canadian Dollars, with CAD payment rails and no FX markups on domestic spend

- No Personal Guarantee: Underwriting based on business cash balance, not founder's personal credit

- Spend Controls: Per-card limits, merchant restrictions, and approval workflows comparable to US fintech leaders

- Receipt Capture + Auto-Categorization: Email forwarding and mobile capture with AI categorization for Canadian tax compliance

- QuickBooks + Xero Integration: Real-time sync with the two accounting systems dominant in Canadian startups

Pricing & Rewards

| Detail | Rate / Fee | Notes |

|---|---|---|

| Float Essentials | Free | Free (core platform) |

| Float Plus | $10 CAD | $10 CAD per user/mo |

| Cashback Rewards | 1% | 1% on all CAD spend |

Pros

- Best fintech-native corporate card for Canadian startups, with no real US-equivalent issue

- CAD-denominated operations save 2-3% FX costs versus using US cards

- Spend management feature parity with Mercury and Rho

- Strong QuickBooks Online and Xero integrations matching Canadian SMB stack

Cons

- Canada-only — not useful for US-only operations

- Cashback rate (1%) below US fintech leaders

- Smaller card network reach than AMEX or Visa Business

Verdict: If you're a Canadian-incorporated startup, Float is the obvious pick. No alternative offers the same combination of CAD-native operations, no personal guarantee, and modern spend management features.

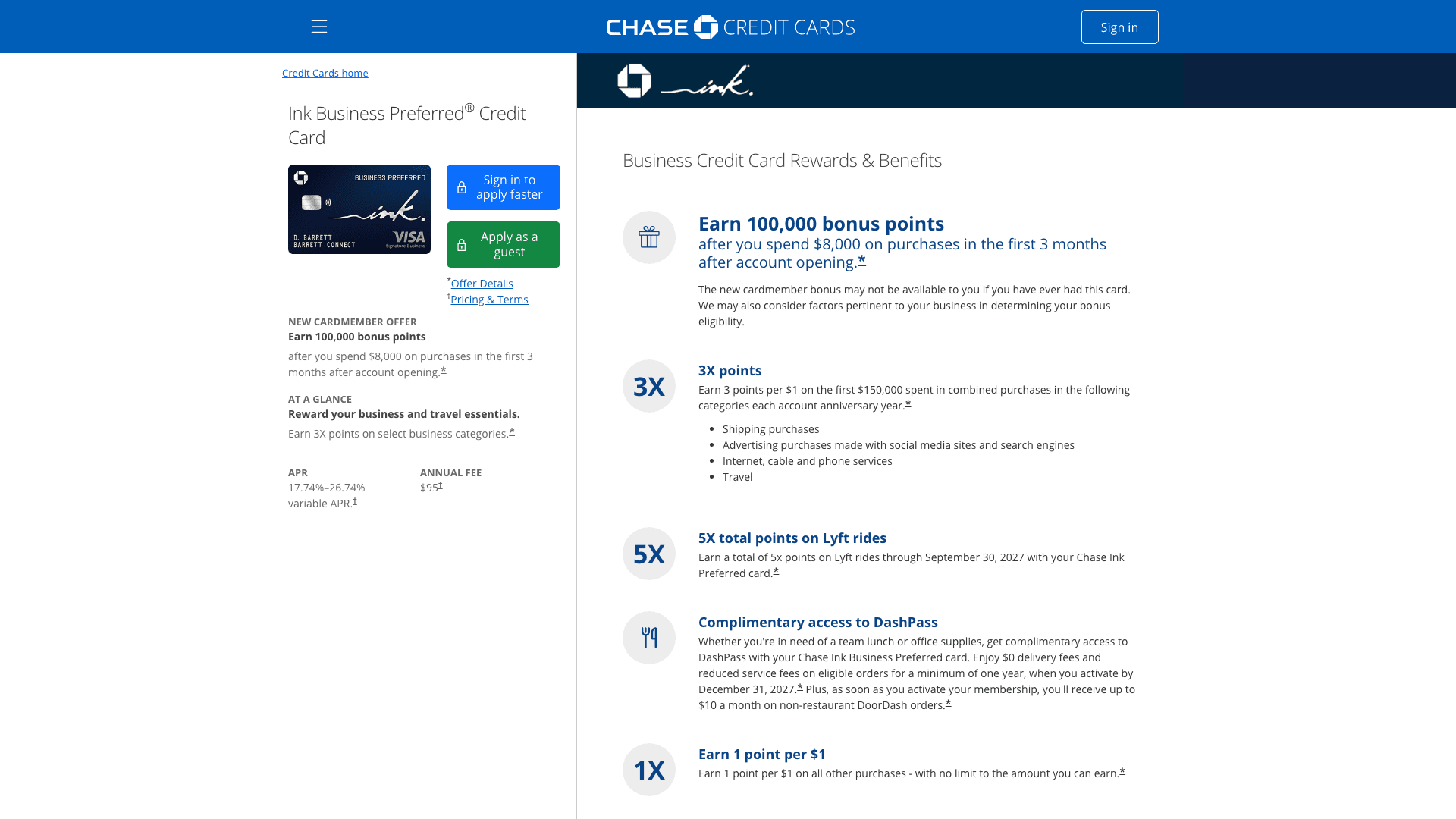

Visit FloatChase Ink Business Preferred

Best for: Established businesses spending heavily on travel, shipping, internet/cable/phone, and online advertising

Chase Ink Business Preferred is the points card that earns its place when the AMEX Business Platinum's $695 annual fee feels excessive but you still want category-targeted rewards. $95 annual fee, 3x points on travel, shipping, internet/cable/phone, and online advertising (capped at $150K combined annually), and points transferable to Chase Ultimate Rewards travel partners (United, Hyatt, Southwest, etc.) at full 1:1 value. For startups spending heavily on paid acquisition (Google Ads, Meta Ads, LinkedIn Ads all count) and shipping (DTC startups, B2B SaaS sending swag), the 3x category match is exceptional value.

Key Features

- 3x Business Categories: 3 Ultimate Rewards points per dollar on travel, shipping, internet/cable/phone, and online advertising up to $150K annually

- Chase Travel Portal: 25% bonus on points redeemed for travel through Chase Travel, plus 1:1 transfer to United, Hyatt, Southwest, and more

- Welcome Bonus: 100,000 Ultimate Rewards points after qualifying spend in the first 3 months — worth $1,250+ in travel

- Free Employee Cards: Unlimited employee cards with individual spend limits, all earning the same rewards

- Cell Phone Protection: Up to $1,000 in cell phone theft and damage protection when bill paid with card

Pricing & Rewards

| Detail | Rate / Fee | Notes |

|---|---|---|

| Annual Fee | $95 | $95/yr |

| Travel Rewards | 3x | 3x on travel, shipping, internet, ads |

| Signup Bonus | 100K | 100K points after qualifying spend |

Pros

- Best points-per-dollar in business categories that matter to most startups

- Online advertising category catches Google Ads, Meta Ads, LinkedIn Ads spend

- Ultimate Rewards transfer partners include United, Hyatt, and Southwest at 1:1

- $95 annual fee accessible for early-stage businesses

Cons

- Personal guarantee required

- $150K annual cap on 3x categories limits scale benefit

- Maximizing points requires deliberate redemption optimization

- Approval requires established personal credit

Verdict: Chase Ink Business Preferred is the right call when you're spending 5-figures monthly on paid acquisition and travel and want category-matched points. The $95 fee makes it more accessible than AMEX Business Platinum.

Visit Chase Ink Business PreferredNavan Connect

Best for: Travel-heavy startups that want corporate cards bundled with travel booking and expense management

Navan Connect (the corporate card layer on top of Navan's travel management platform, formerly TripActions) is the right pick when business travel is a meaningful share of company spend and you want booking, cards, and expense reconciliation in one system. Book flights and hotels through Navan, transactions flow straight to the corporate card, expenses auto-categorize, and reconciliation happens without any receipt chasing. For startups with 5+ employees traveling regularly — sales teams, customer success doing onsite visits, founders doing investor circuits — the consolidation pays off in saved finance team hours and better travel policy enforcement.

Key Features

- Travel + Card Integration: Book through Navan, transaction auto-applies to Navan-issued corporate card with full reconciliation

- Smart Spend Policies: AI-powered policy enforcement during booking — agents see in-policy options first, exceptions flagged automatically

- Real-Time Expense Reports: Expenses categorized and approved as they happen, not days after the trip

- Global Card Issuance: Corporate cards in USD, EUR, GBP, and major global currencies with no foreign transaction markup on travel

- AP + Cards Combined: Same platform handles travel cards, non-travel cards, and vendor invoice payments

Pricing & Rewards

| Detail | Rate / Fee | Notes |

|---|---|---|

| Navan Platform | Free | Free for travel + expense module |

| Navan Connect Cards | Free | Free corporate cards with platform |

| Cashback / Travel Credits | Variable | Travel credits earned via booking platform |

Pros

- Best travel-and-card integration available — booking and spend happen in one workflow

- AI policy enforcement reduces out-of-policy spend by 60%+ in most deployments

- Free platform unusual at this level of feature depth

- Global card issuance solves multi-currency travel pain

Cons

- Only justifies if travel is meaningful share of spend (10%+)

- Less competitive on cashback than dedicated fintech cards

- Smaller spend management focus outside travel context

- Platform optimized for travel-heavy teams, not general spend

Verdict: Navan Connect is the right call when travel is a real spend category for your team. Pair with Mercury or Rho for general operations spend; Navan owns the travel-and-card lane.

Visit Navan ConnectCorporate Card Categories

The 10 cards above fall into four distinct categories, each optimized for different startup workflows. Understanding which category fits your team is more important than chasing the single highest-rated card:

Fintech-native cards (Mercury, Rho, Float) bundle banking and cards in one platform — the right pick for most VC-backed startups. Traditional bank cards (AMEX, Capital One, Chase) deliver rewards programs but require personal guarantees and lack modern spend controls. Spend management platforms (Bill, Airbase, Stripe) wrap cards inside broader finance workflows — useful when finance team operations matter more than card rewards. Travel and expense platforms (Navan) bundle booking with cards for travel-heavy teams.

How to Choose for Your Startup

Beyond category, the right pick depends on your funding stage, spend pattern, integration needs, and team size. Here's the decision framework:

If you're a pre-seed or seed-stage startup with funding in the bank...

Choose Mercury. The IO Card with no annual fee, no personal guarantee, and 1.5%-2.5% cashback lives on top of the banking account you'd want anyway. One platform, no friction.

If you're growth-stage and need banking, AP, treasury, and cards in one platform...

Choose Rho. The integrated finance platform reduces operational overhead meaningfully once you have a real finance function, and the treasury management features genuinely de-risk larger cash positions.

If you have 10+ employees needing cards on a tight budget...

Choose Bill Spend & Expense. The combination of free platform + deep accounting integrations + mature approval workflows is unmatched at this price.

If your team travels heavily (10%+ of spend)...

Choose Navan Connect for the booking-and-card integration, or AMEX Business Platinum for the founder/exec line if maximizing travel rewards matters.

If you're a developer-first company that wants programmable cards...

Choose Stripe Issuing. Treat cards as infrastructure rather than a UI — API-issued virtual cards with webhook-driven authorization unlock genuinely novel workflows.

If you want simple flat cashback from a traditional bank...

Choose Capital One Spark Cash Plus. 2% on everything, no foreign transaction fees, no points game. Best for established businesses with strong personal credit.

Pro Tip

Most startups need exactly one corporate card platform — not three. The reconciliation pain of running multiple providers usually outweighs any reward optimization. Pick one fintech-native card for primary spend, and consider adding a single rewards card (AMEX or Chase) only if travel justifies it.

Frequently Asked Questions

Final Thoughts

The best corporate card for your startup depends on your stage, your spend pattern, and your finance team's bandwidth — not on which card has the most viral marketing. For most VC-backed startups, the right move is straightforward: open Mercury for banking-plus-cards on day one, and stay with it until growth-stage finance complexity justifies upgrading to Rho's full integrated platform. Add a traditional rewards card only if your team's travel or paid acquisition spend makes the points math obvious.

The single biggest mistake we see is founders chasing the highest cashback rate or most exotic feature set when the operational realities (reconciliation pain, multi-platform overhead, personal guarantee exposure) dwarf any reward optimization. Pick one fintech-native platform that fits your stage, wire it into your accounting system on day one, and treat corporate cards as boring infrastructure — that's how you free up the cycles to build the actual product.

Related Free SEO Tools

Content Brief Generator

Generate SERP-grounded briefs for your category content

SEO Content Grader

Score your comparison and alternative pages

Meta Tags Generator

Optimize SERP previews for landing pages

Long-Tail Keyword Generator

Find low-competition commercial queries

Keyword Extractor

Pull keywords from competitor pages

Content Outline Generator

Structure BOFU content for ranking

Related Articles

Best AI SEO Tools for SaaS Companies

The SEO stack for SaaS startups in 2026

Best AI SEO Tools for Small Businesses

Budget-friendly tools that deliver real ROI

Best AI SEO Tools for Keyword Research

Find ranking opportunities competitors miss

Browse All Articles

Explore our complete library of guides and tutorials

About the Author

Co-Founder & SEO Execution

Co-founder of PikaSEO. 11 years in corporate tech, then bootstrapped entrepreneur. Leads SEO execution and content-led growth for SaaS companies.