“Business banking for startups” is a slightly misleading phrase, and understanding why is the first step to choosing well. Most of the platforms founders reach for — Mercury, Rho, Relay, Novo, Found, North One — are not banks at all. They are financial technology companies that partner with FDIC-member banks: the bank holds your deposits and provides the insurance, while the fintech builds the software, the cards, and the treasury features on top. The experience feels like banking, and it is usually better software than a traditional bank offers, but the charter — and the direct relationship — sits one layer removed.

That nuance matters because it shapes the two things a startup cares about most: how safe the money is, and how much it costs to move. FDIC insurance passes through the partner bank, so the health of that bank and the accuracy of the fintech's ledger both matter — a lesson the 2024 Synapse middleware collapse taught the hard way. The best platforms mitigate this with sweep networks that spread balances across many partner banks to expand FDIC coverage well beyond the standard $250,000. Meanwhile “no monthly fee” is nearly universal and mostly honest, but the real cost hides in wire fees, foreign-exchange markups, and ACH limits.

This guide ranks the 10 startup banking providers we'd actually shortlist in 2026, organized by the job each is best at — with honest positioning about the fintech-versus-chartered distinction. We evaluated each on four criteria: FDIC coverage and safety (partner-bank structure, sweep networks, and how far insurance extends), fees and real cost (monthly fees, wires, FX, and ACH limits at realistic volumes), integrations and bookkeeping (accounting sync, invoicing, and cash-organization tools), and startup fit and scale (whether it suits a fresh venture raise, a bootstrapped SMB, or a solo founder).

Quick Comparison: The Best Startup Business Banking at a Glance

| Provider | Best For | Monthly Fee | FDIC Model | Standout |

|---|---|---|---|---|

| Mercury | Best Overall for Startups | $0 | Fintech + sweep network | Expanded FDIC + treasury |

| Rho | Banking + Spend Combo | $0 | Fintech + sweep network | Waived wires, cards, AP |

| Relay | Cash Management & Bookkeeping | $0 (Pro ~$30) | Fintech + partner bank | Up to 20 accounts |

| Bluevine | Earning Interest | $0 (paid tiers) | Fintech + partner bank | APY on checking |

| Arc | Venture-Backed Startups | $0 | Fintech + sweep network | Treasury + venture debt |

| Novo | Small Businesses & Freelancers | $0 | Fintech + partner bank | Free + invoicing |

| Found | Self-Employed & Solopreneurs | $0 (Plus ~$20) | Fintech + partner bank | Auto tax estimates |

| North One | Budgeting & Cash Control | ~$10/mo | Fintech + partner bank | Envelope budgeting |

| Grasshopper | Chartered Digital Bank | $0 | Chartered (direct FDIC) | Real bank charter |

| Wise Business | International & Multi-Currency | $0 (setup fee) | E-money / safeguarded | Cheap multi-currency FX |

How We Evaluated the Best Startup Business Banking

Every platform advertises a clean app and “no monthly fees.” We weighted the dimensions that actually separate providers once your company's money is sitting in the account:

FDIC Coverage & Safety

Most providers are fintechs over partner banks, so we scored the coverage structure: which banks hold deposits, whether a sweep network expands FDIC insurance beyond $250,000, and whether the platform is a chartered bank with direct insurance.

Fees & Real Cost

“No monthly fee” hides the real economics. We looked past the headline at domestic and international wire fees, FX markups on cross-border payments, ACH limits, and minimum balances — the line items that decide what you actually pay.

Integrations & Bookkeeping

A business account lives next to your accounting stack. We weighted QuickBooks and Xero sync depth, invoicing, tax tooling, and cash-organization features like sub-accounts and envelopes that keep the books clean without extra software.

Startup Fit & Scale

A fresh venture raise, a bootstrapped SMB, and a solo freelancer need different things. We scored each provider for the stage it truly fits — runway treasury and expanded FDIC for the funded, simplicity and tax help for the solo operator.

Pro Tip

Before comparing providers, confirm which FDIC-member bank actually holds the deposits and how pass-through insurance is structured — it's in every fintech's disclosures. For balances above $250,000, verify the current sweep-network coverage limit and which banks participate. If middleware risk worries you at all, keep a portion of reserves at a chartered bank like Grasshopper or in a brokerage account.

Fees at a Glance

The headline is that almost every startup banking platform charges $0 a month — so the monthly fee is rarely the deciding factor. What separates them is the standout capability each is built around, and the transaction costs (wires, FX, ACH) beneath the free label. Here's the field on one axis, colored by segment:

The Best Startup Banking Providers, by Category

Before reading individual reviews, place your company on this map — your funding stage and how you manage cash narrow ten providers to a shortlist of two or three:

Venture-backed startup banks (Mercury, Arc, Rho) expand FDIC coverage through sweep networks and put idle runway into treasury yield — the right home for a fresh raise. SMB and cash-management fintechs (Relay, Bluevine, North One) win on multi-account structure, envelope budgeting, and interest — built for bootstrapped businesses running on operating cash. Solo and freelancer accounts (Novo, Found) strip banking down to a free, simple account with invoicing, bookkeeping, and automatic tax set-aside. Chartered and global providers (Grasshopper, Wise Business) cover the two edge cases the fintechs handle least well: a genuine bank charter with direct FDIC, and cheap multi-currency banking for cross-border teams.

Mercury

Best for: Venture-backed and scaling startups that want a clean operating account, expanded FDIC coverage, treasury yield, cards, and bill pay in one modern platform

Mercury has become the default banking platform for startups, and it earns the top spot by doing the fundamentals cleanly while stacking real depth on top. The core is a genuinely pleasant operating account — free, fast to open online, with no monthly fees and no minimums — but the reason startups pick it is coverage and consolidation. Mercury's sweep network spreads balances across many partner banks to expand FDIC coverage into the millions, and its treasury product puts idle runway into money-market funds so cash earns yield without leaving the platform. Around that sit corporate cards with cashback, bill pay, and a well-regarded API. The honest nuance: Mercury is a fintech, not a chartered bank — deposits are held by partner banks (Choice Financial, Column, and others) with FDIC insurance passing through, so the partner banks' health and Mercury's ledger accuracy both matter. It is US-centric, and international coverage, while improving, is not its strength.

Key Features

- Free Operating Account: No monthly fees, no minimums, and online setup in minutes with your EIN and formation docs

- Sweep-Expanded FDIC Coverage: Balances distributed across partner banks to extend FDIC insurance well beyond $250,000

- Treasury with Yield: Idle runway swept into money-market funds so cash earns while staying accessible

- Corporate Cards & Bill Pay: Cashback cards with spend controls plus built-in accounts payable

- Developer API & Integrations: Well-regarded API and QuickBooks/Xero sync for programmatic finance ops

Pricing

| Plan | Monthly | Annual (per month) |

|---|---|---|

| Mercury (banking) | $0 | $0 (no monthly fees) |

| Mercury Plus | ~$35 | ~$35/mo (added invoicing/tools) |

| Mercury Pro | ~$350 | ~$350/mo (scaling teams) |

Pros

- Best-in-class UX and fast online onboarding for startups

- Sweep network expands FDIC coverage into the millions

- Treasury yield and cards consolidated in one platform

- Strong API and accounting integrations

Cons

- A fintech, not a chartered bank — deposits held at partner banks

- US-centric with limited international/multi-currency depth

- No physical branches or cash-deposit network

Related reading: Best Treasury & Cash Management Software

Verdict: Mercury is the best startup banking platform for most companies in 2026. If you want a clean operating account with expanded FDIC coverage and treasury built in, start here — it scales from pre-seed to Series C without a migration.

Visit MercuryRho

Best for: Startups and growth-stage teams that want business banking, corporate cards, AP, and treasury consolidated into one free, white-glove platform

Rho's pitch is consolidation at zero software cost: business checking and treasury, corporate cards with cashback, accounts payable, and expense management in a single platform, monetized through interchange and banking economics rather than subscriptions. For teams tired of stitching a bank, a card program, and an AP tool together, Rho collapses the stack into one vendor with a notably hands-on support model — named account teams are part of the pitch even on the free tier. It waives most wire fees, which matters for companies moving money frequently, and its treasury product puts idle cash to work. Like Mercury, Rho is a fintech partnered with FDIC-member banks rather than a chartered bank itself, and it runs a sweep program to expand coverage. The trades: it is US-centric, the full value assumes you move banking and card spend onto the platform, and it leans toward funded startups and established SMBs over the smallest solo operations.

Key Features

- Banking + Cards + AP + Treasury: One platform and support relationship replaces a multi-vendor finance stack

- No Monthly Fees, Waived Wires: Free platform with most domestic and international wire fees waived

- Corporate Cards with Cashback: Physical and virtual cards with real-time spend controls and rewards

- Treasury & Sweep Coverage: Idle cash earns yield; sweep network extends FDIC coverage across partner banks

- White-Glove Support: Named account teams and onboarding help unusual at a free price point

Pricing

| Plan | Monthly | Annual (per month) |

|---|---|---|

| Rho platform (banking, cards, AP) | $0 | $0 (interchange/banking-funded) |

| Treasury management | Included | Included |

Pros

- Whole finance stack — bank, cards, AP, treasury — in one free platform

- Most wire fees waived, unusual for the category

- White-glove support even on the free tier

- Cashback cards with genuine policy controls

Cons

- A fintech partnered with banks, not a chartered bank

- US-centric with limited international depth

- Full value requires moving banking and cards over

Related reading: Best Corporate Cards for Startups

Verdict: Rho is the consolidation pick. If you want your bank, cards, AP, and treasury under one roof with waived wires and hands-on support, it delivers a genuinely strong platform for free.

Visit RhoRelay

Best for: Small businesses and bookkeeper-led teams that manage cash with multiple accounts, envelope budgeting, and deep accounting sync

Relay is built for a specific and underserved job: managing cash across many accounts with discipline. You can open up to 20 individual checking accounts and 50 virtual cards, which makes cash-allocation methods like Profit First or envelope budgeting native rather than a workaround — payroll here, taxes there, operating expenses somewhere else, each in its own account. That structure, plus deep two-way sync with QuickBooks Online and Xero, has made Relay a favorite of bookkeepers and accountants managing multiple clients. It is a fintech partnered with FDIC-member banks (Thread Bank), not a chartered bank, and its free plan covers the core; a paid Pro tier adds faster same-day ACH, wires, and auto-transfer rules. The trades: it is less focused on venture-scale treasury and expanded-FDIC sweeps than Mercury or Rho, and its strength is organization and bookkeeping rather than maximizing yield on a large raise.

Key Features

- Up to 20 Checking Accounts: Native multi-account structure for Profit First, envelopes, and cash allocation

- 50 Virtual & Physical Cards: Per-purpose cards with individual limits for team and vendor spend

- Deep QuickBooks & Xero Sync: Two-way accounting sync bookkeepers rely on for clean reconciliation

- Auto-Transfer Rules: Percentage-based rules move money into the right accounts automatically

- Bookkeeper-Friendly Access: Role-based access built for accountants managing multiple clients

Pricing

| Plan | Monthly | Annual (per month) |

|---|---|---|

| Relay (free) | $0 | $0 |

| Relay Pro | ~$30 | ~$30/mo (same-day ACH, auto-transfers) |

Pros

- Up to 20 accounts make cash-allocation methods native

- Best-in-class QuickBooks and Xero sync for bookkeepers

- Free core plan with no minimums

- Virtual cards and auto-transfer rules for real cash control

Cons

- A fintech partnered with a bank, not a chartered bank

- Less treasury/yield depth than venture-focused platforms

- Faster payments and automation sit behind the Pro tier

Related reading: Best Expense Management Tools

Verdict: Relay is the cash-management and bookkeeping pick. If you run your business by allocating cash across accounts and live in QuickBooks or Xero, nothing else on this list fits that workflow as naturally.

Visit RelayBluevine

Best for: Small businesses that keep meaningful operating balances and want to earn a competitive APY on checking, with lending available alongside

Bluevine's differentiator is yield on your checking balance. Where most startup banking platforms pay nothing on the operating account (steering you to a separate treasury product), Bluevine pays a competitive APY on business checking — historically on balances up to a cap and subject to activity requirements — which makes it attractive for SMBs that hold cash in the account rather than sweeping it out. Beyond interest, Bluevine leans into lending: it offers business lines of credit and financing, so it doubles as a capital source for growing small businesses. It is a fintech partnered with FDIC-member banks (Coastal Community Bank), with sweep options to expand coverage. The trades: the headline APY typically applies only up to a balance cap and requires meeting monthly activity thresholds (minimum spend or deposit), the tiered plans add monthly fees for higher limits, and it is oriented toward SMBs rather than venture-scale treasury management.

Key Features

- Interest on Checking: Competitive APY on business checking balances up to a cap, subject to activity rules

- Business Lines of Credit: Integrated lending and financing for growing small businesses

- Sweep FDIC Expansion: Optional deposit network to extend FDIC coverage beyond the standard limit

- Payments & Bill Pay: ACH, wires, and bill pay with sub-accounts for organizing cash

- Accounting Integrations: QuickBooks, Xero, and other sync options for reconciliation

Pricing

| Plan | Monthly | Annual (per month) |

|---|---|---|

| Standard | $0 | $0 (APY with activity thresholds) |

| Plus | ~$30 | ~$30/mo (higher limits/APY) |

| Premier | ~$95 | ~$95/mo (top tier) |

Pros

- Earns competitive APY directly on checking balances

- Integrated lines of credit and financing

- Free standard plan available

- Sub-accounts and sweep coverage for cash organization

Cons

- APY typically capped and gated behind monthly activity rules

- Higher limits and APY require paid tiers

- SMB-oriented, not built for venture-scale treasury

Verdict: Bluevine is the interest pick. If you keep real cash in your operating account and want it earning without moving to a separate treasury product — plus access to a credit line — it is the strongest fit.

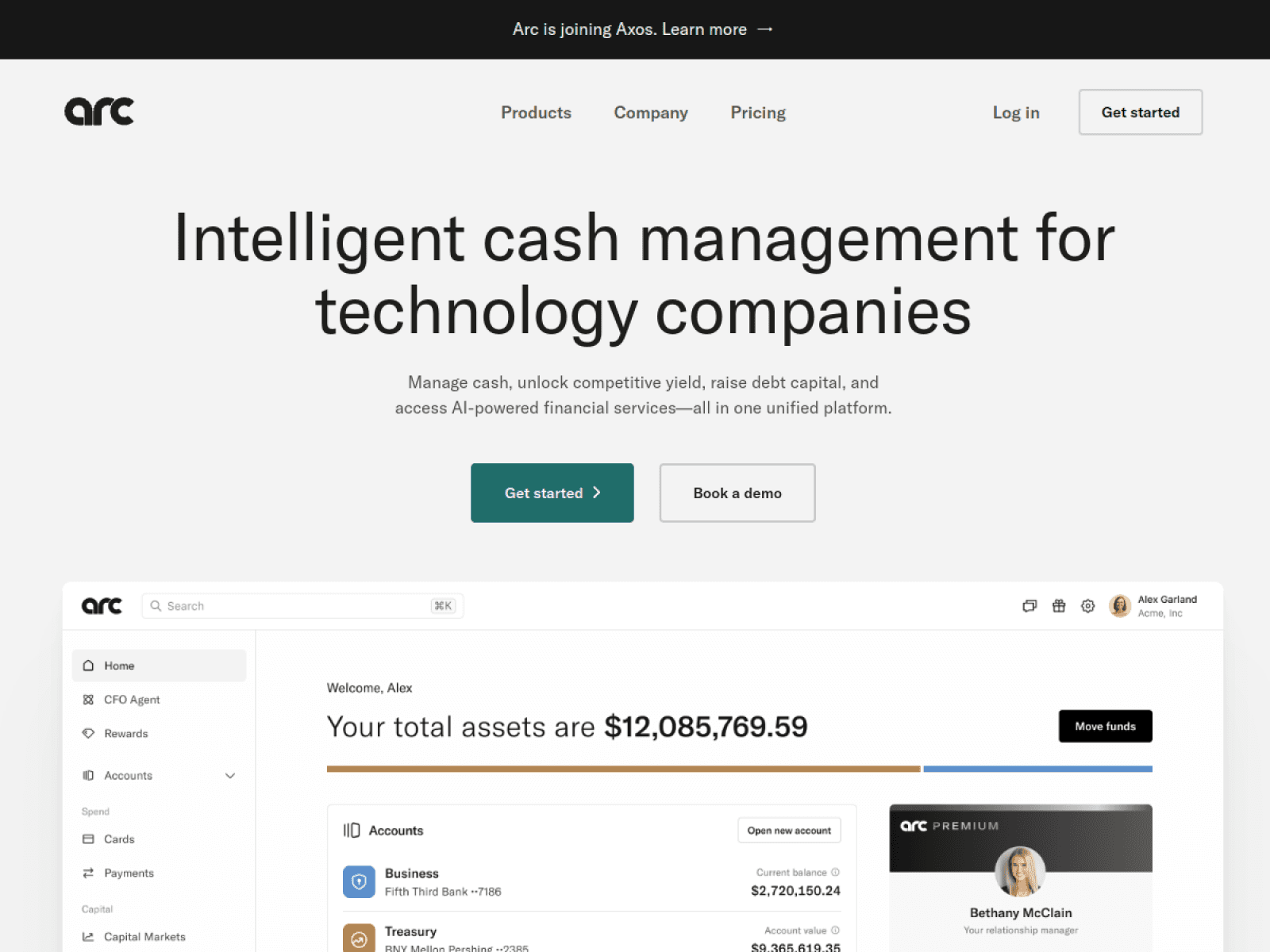

Visit BluevineArc

Best for: Venture-backed startups that want banking, treasury, and access to venture debt and financing in one platform built for the funding cycle

Arc is built specifically for the venture-backed company managing a fresh raise. It combines a business banking layer with treasury — sweep-based FDIC expansion and money-market yield on idle runway — and, distinctively, integrated access to venture debt and financing. For a startup that has just raised, the pitch is compelling: park runway somewhere it is both insured beyond $250,000 and earning, then tap non-dilutive debt through the same platform when you want to extend runway without another equity round. Arc is a fintech partnered with FDIC-member banks rather than a chartered bank, and it is deliberately narrow — it is aimed at funded, higher-growth companies, not bootstrapped small businesses or solo founders. The trades: it is less relevant if you are not raising or holding significant cash, its everyday banking feature set is leaner than Mercury's, and the financing side involves underwriting and is not guaranteed.

Key Features

- Treasury for Runway: Money-market yield on idle cash with sweep-based FDIC expansion

- Venture Debt & Financing: Integrated access to non-dilutive capital to extend runway

- Business Banking Layer: Operating accounts and payments built around the funding cycle

- Expanded FDIC Coverage: Deposit network spreads balances across partner banks beyond $250,000

- Startup-Focused Onboarding: Designed for venture-backed cap tables and post-raise cash management

Pricing

| Plan | Monthly | Annual (per month) |

|---|---|---|

| Arc (banking + treasury) | $0 | $0 (no platform fee) |

| Financing / venture debt | Underwritten | Rate-based (varies) |

Pros

- Purpose-built for post-raise runway management

- Treasury yield plus expanded FDIC coverage

- Integrated venture debt for non-dilutive runway

- Clean fit for venture-backed cap tables

Cons

- A fintech partnered with banks, not a chartered bank

- Narrow fit — little value for bootstrapped or solo founders

- Everyday banking features leaner than Mercury's

Related reading: Best Treasury & Cash Management Software

Verdict: Arc is the venture-backed pick. If you have just raised and want runway insured, earning, and financeable in one place, it is built for exactly that moment — pair it with a primary operating account.

Visit ArcNovo

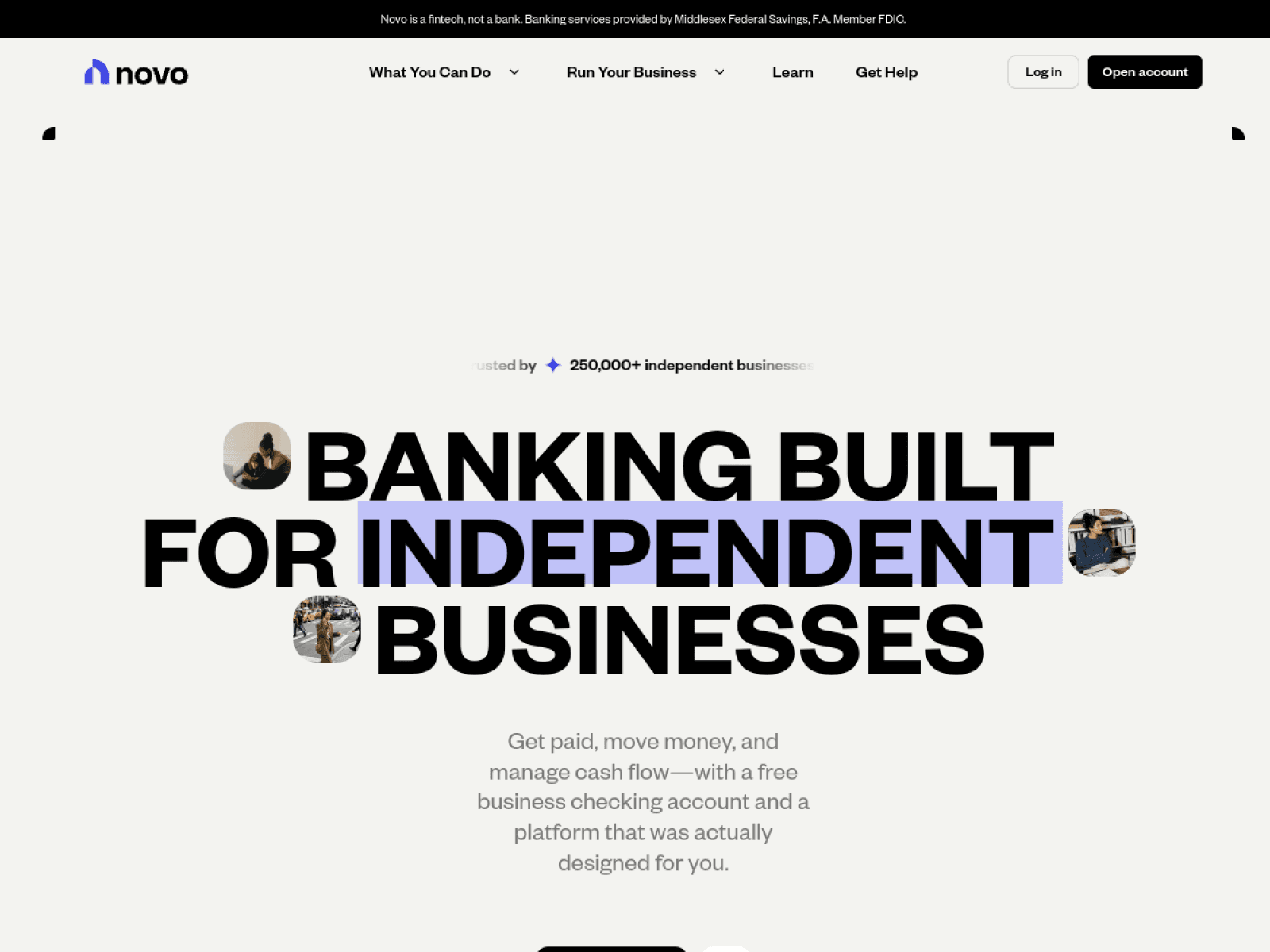

Best for: Bootstrapped small businesses, freelancers, and early founders who want a free, simple checking account with invoicing and integrations

Novo is the no-friction choice for small businesses that want a clean checking account without fees, minimums, or complexity. It is free — no monthly fee, no minimum balance — and opens online in minutes, which makes it a popular first business account for freelancers, e-commerce sellers, and early founders. The product is deliberately simple: a solid operating account, free invoicing to get paid, integrations with tools like Stripe, Shopify, and QuickBooks, and Novo Reserves for setting aside money into sub-accounts (for taxes or goals). It is a fintech partnered with an FDIC-member bank (Middlesex Federal Savings), not a chartered bank. The trades follow from the simplicity: there is no meaningful interest on balances, no expanded-FDIC sweep network for large deposits, and no corporate-card program or treasury — it is built for small operating balances and everyday cash flow, not for parking a venture raise.

Key Features

- Free Business Checking: No monthly fees, no minimum balance, online setup in minutes

- Built-In Invoicing: Create and send invoices and get paid directly into the account

- Novo Reserves: Set-aside sub-accounts for taxes, payroll, or savings goals

- Integrations: Connects to Stripe, Shopify, QuickBooks, and other small-business tools

- Fee Refunds: Refunds ATM fees, a nice touch for a free account

Pricing

| Plan | Monthly | Annual (per month) |

|---|---|---|

| Novo (business checking) | $0 | $0 (no monthly fees, no minimums) |

Pros

- Genuinely free with no minimums

- Fast online onboarding for freelancers and early founders

- Free invoicing and useful small-business integrations

- Reserves sub-accounts for setting money aside

Cons

- No meaningful interest on balances

- No expanded-FDIC sweep for large deposits

- No corporate cards or treasury — built for small balances

Verdict: Novo is the small-business and freelancer pick. If you want a free, simple, get-paid-and-go checking account without treasury complexity, it is one of the easiest accounts to open and run.

Visit NovoFound

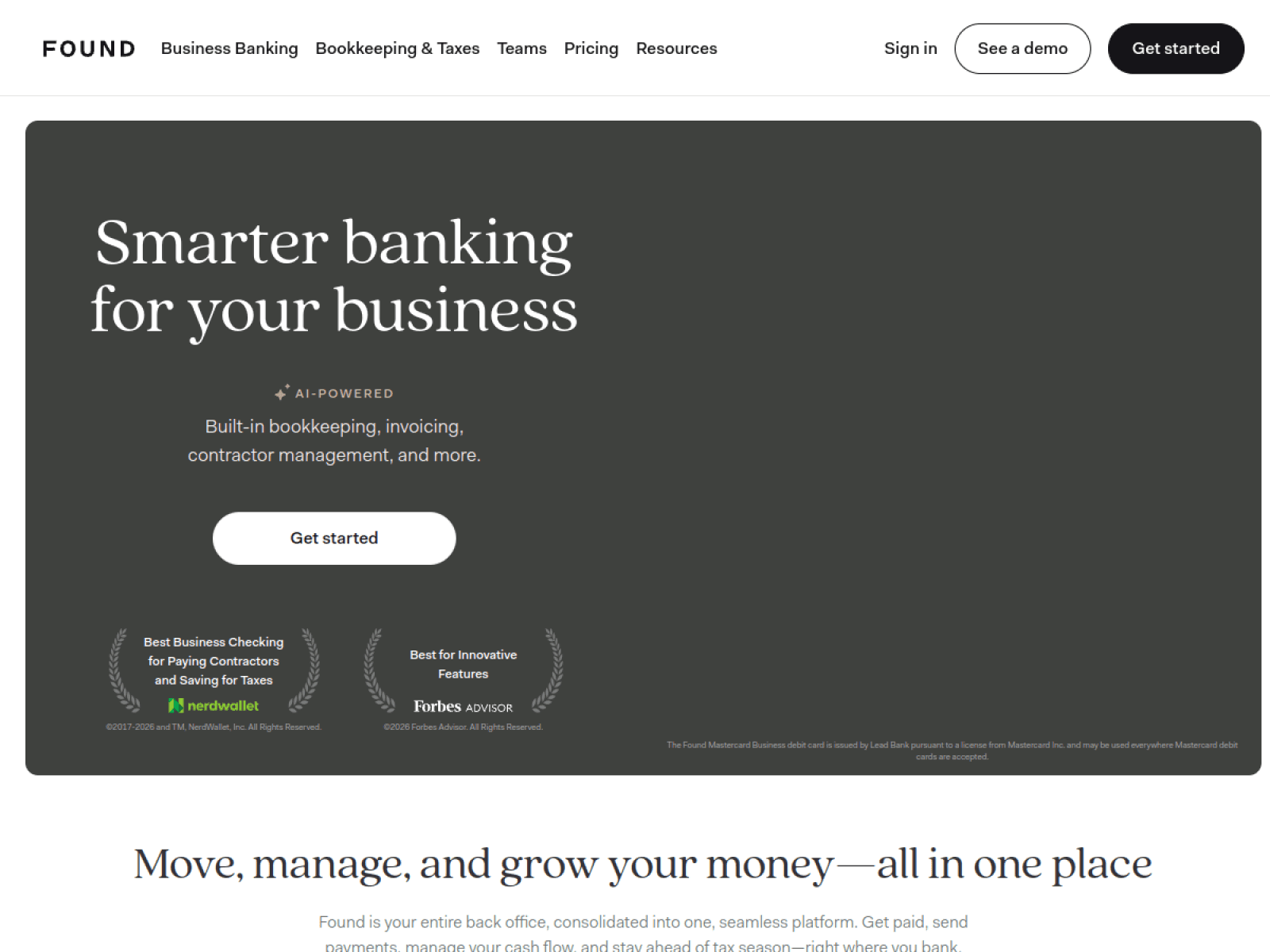

Best for: Freelancers, sole proprietors, and one-person businesses that want banking with bookkeeping and automatic tax estimates built in

Found is banking designed around the reality of being self-employed: you are also your own bookkeeper and tax department. It bundles a free business checking account with built-in expense tracking, invoicing, and — the standout — automatic tax estimation that sets aside what you owe as income comes in, so quarterly estimated taxes stop being a surprise. For a freelancer or sole proprietor who would otherwise juggle a bank, a spreadsheet, and a shoebox of receipts, Found collapses all three into one app. It is a fintech partnered with an FDIC-member bank (Piermont Bank), not a chartered bank. The trades reflect its focus: it is built for solo operators and very small businesses, so it lacks the multi-user controls, corporate cards, treasury, and expanded-FDIC sweeps that funded startups need, and a paid Found Plus tier unlocks faster transfers and advanced features. For a team raising venture capital it is the wrong tool; for a one-person business it is close to ideal.

Key Features

- Free Checking for the Self-Employed: No monthly fee account built for freelancers and sole proprietors

- Automatic Tax Estimates: Sets aside estimated taxes as income arrives so quarterlies aren't a surprise

- Built-In Bookkeeping: Automatic expense categorization and Schedule C-friendly reporting

- Invoicing: Send invoices and accept payments directly into the account

- Found Plus: Optional paid tier for faster transfers and advanced tax/bookkeeping tools

Pricing

| Plan | Monthly | Annual (per month) |

|---|---|---|

| Found (core) | $0 | $0 (no monthly fees) |

| Found Plus | ~$20 (or ~$150/yr) | ~$12.50/mo billed annually |

Pros

- Automatic tax set-aside built for the self-employed

- Bookkeeping and invoicing bundled into the account

- Free core plan with no minimums

- Genuinely reduces admin for solo operators

Cons

- Built for solopreneurs — no multi-user or corporate cards

- No treasury or expanded-FDIC sweep for large balances

- Advanced features gated behind Found Plus

Verdict: Found is the solopreneur pick. If you are a freelancer or sole proprietor who dreads bookkeeping and quarterly taxes, its automatic tax estimation alone can justify the switch.

Visit FoundNorth One

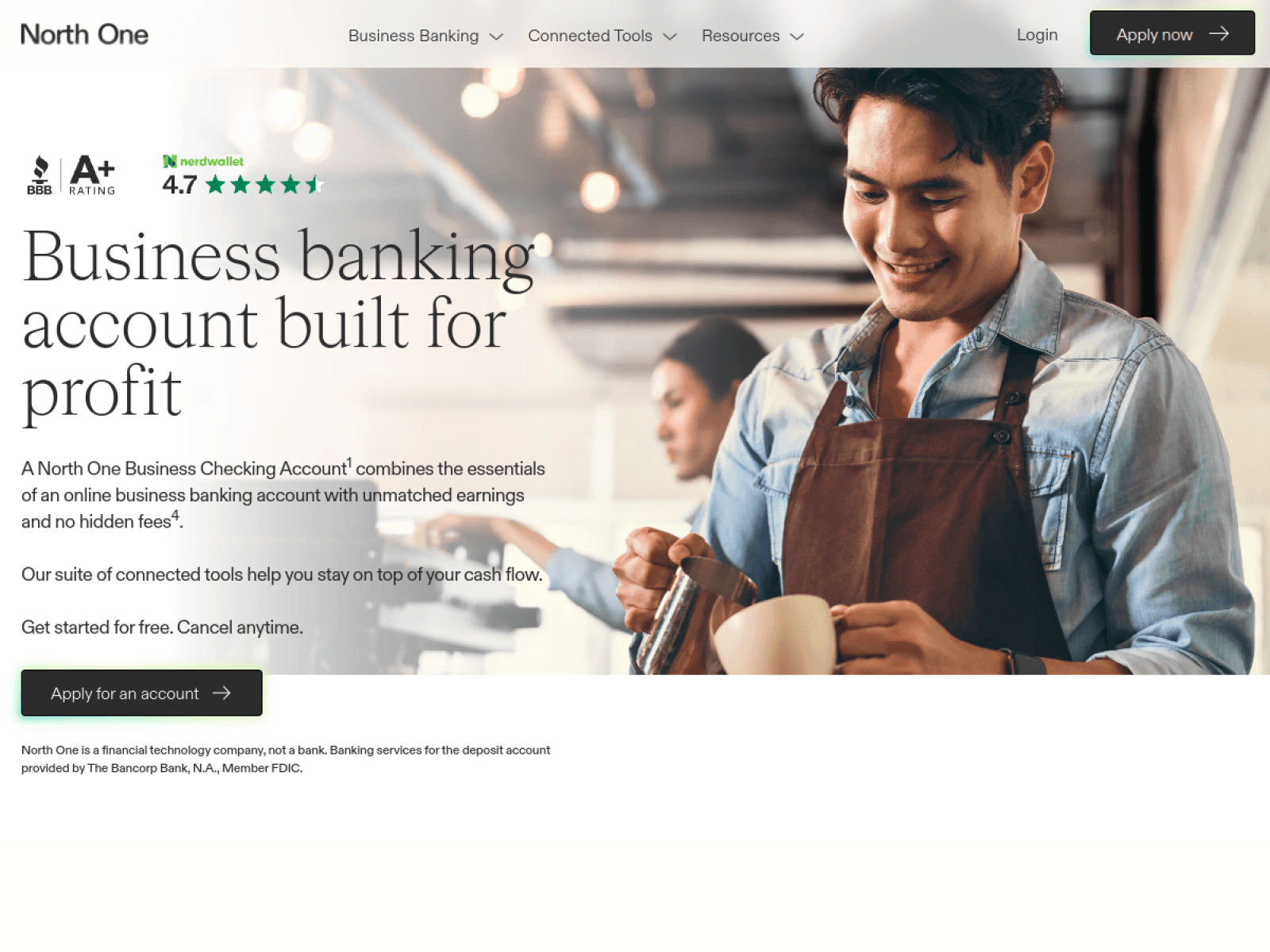

Best for: Small businesses that want envelope-style budgeting and disciplined cash control in a simple, integration-friendly account

North One is built around budgeting discipline for small businesses. Its signature feature, Envelopes, lets you carve your balance into virtual buckets — taxes, payroll, rent, operating expenses — so money is allocated before it is spent rather than tracked after the fact, similar in spirit to Relay's multi-account approach but delivered as budget envelopes within an account. That makes it a strong fit for owner-operators who want to see, at a glance, that the tax money is set aside and payroll is covered. It rounds out with integrations (QuickBooks, Stripe, Shopify, PayPal) and standard payments. North One is a fintech partnered with an FDIC-member bank, not a chartered bank. It charges a modest monthly fee on its main plan (unlike the strictly-free options), and the trades are that it is SMB-focused — no venture-scale treasury, no expanded-FDIC sweep network, and a feature set aimed at cash control rather than yield or scale.

Key Features

- Envelope Budgeting: Carve your balance into virtual buckets so money is allocated before it's spent

- Small-Business Payments: ACH, wires, mobile deposit, and bill pay in a simple interface

- Integrations: Connects to QuickBooks, Stripe, Shopify, PayPal, and more

- Sub-Account Structure: Organize cash by purpose without opening separate accounts

- Cash Flow Visibility: See at a glance that taxes and payroll are covered before spending

Pricing

| Plan | Monthly | Annual (per month) |

|---|---|---|

| Standard | ~$10 | ~$10/mo |

| Plus | ~$20 | ~$20/mo (higher limits/features) |

Pros

- Envelope budgeting makes cash control native

- Clean, simple interface for owner-operators

- Solid small-business integrations

- Sub-accounts without opening multiple accounts

Cons

- Monthly fee unlike the strictly-free options

- SMB-focused — no treasury or venture-scale features

- No expanded-FDIC sweep network

Verdict: North One is the budgeting and cash-control pick. If you want the discipline of envelope budgeting baked into your business account, it delivers exactly that for a modest monthly fee.

Visit North OneGrasshopper

Best for: Startups and SMBs that want a real, chartered digital bank — direct FDIC insurance and a genuine banking relationship, not a fintech-over-partner-bank model

Grasshopper is the important exception on this list: it is an actual chartered digital bank, not a fintech riding on partner banks. That distinction matters to founders who are uneasy about the middleware layer between them and a charter — with Grasshopper, your deposits are held directly by an FDIC-insured bank, the relationship is with a regulated institution, and there is no third-party program manager in between. It targets startups, small businesses, and the innovation economy with a modern digital experience: business checking that can earn interest, online-native onboarding, integrations, and access to lending and SBA products that a chartered bank can offer directly. It also participates in deposit networks (such as IntraFi) to extend FDIC coverage beyond $250,000. The trades: as a bank it can be more conservative on onboarding and underwriting than a growth-stage fintech, the product surface is less flashy than Mercury's, and it is a smaller institution than the megabanks — but for founders who specifically want a charter, that is the point.

Key Features

- Chartered, Direct FDIC: A real FDIC-insured bank holds your deposits — no fintech-over-partner-bank layer

- Interest-Bearing Checking: Digital business checking that can earn interest on balances

- Expanded Coverage via IntraFi: Deposit-network participation extends FDIC coverage beyond $250,000

- Lending & SBA Products: A chartered bank can offer loans and SBA financing directly

- Digital-Native Experience: Online onboarding and integrations aimed at the innovation economy

Pricing

| Plan | Monthly | Annual (per month) |

|---|---|---|

| Innovator Checking | $0 | $0 (no monthly fees) |

| Business accounts | Varies | Varies by product |

Pros

- A real chartered bank — deposits held directly, no middleware

- Interest-bearing digital checking

- Direct access to lending and SBA products

- Deposit-network coverage beyond $250,000

Cons

- More conservative onboarding/underwriting than fintechs

- Product surface less feature-rich than Mercury or Rho

- Smaller institution than the megabanks

Verdict: Grasshopper is the chartered-bank pick. If the fintech-over-partner-bank model gives you pause and you want a genuine, regulated banking relationship with a modern digital experience, it is the standout choice.

Visit GrasshopperWise Business

Best for: Startups with cross-border operations that need multi-currency accounts, cheap FX, and low-cost international payments alongside a primary account

Wise Business is the specialist every internationally active startup should hold alongside its primary account. It gives you local account details in multiple currencies — USD, GBP, EUR, AUD, and dozens more — so you can collect from foreign customers as a local, hold balances in several currencies, and pay overseas contractors without the punishing FX markups traditional banks bury in the exchange rate. Wise converts at the real mid-market rate with a small, transparent fee, which routinely beats bank wires and card-network FX by a wide margin. It is not a full-service bank — there is no lending, no US treasury product, and funds are safeguarded rather than FDIC-insured in the US (Wise is an e-money/payments institution, and US balances are held at partner banks with pass-through insurance where applicable) — so it complements rather than replaces an operating account. But for cross-border payments and multi-currency cash, nothing else on this list comes close on cost and breadth.

Key Features

- Multi-Currency Accounts: Local account details in USD, GBP, EUR, and dozens of other currencies

- Mid-Market FX: Currency conversion at the real exchange rate with a small transparent fee

- Cheap International Payments: Cross-border transfers far below traditional bank wire and FX costs

- Global Business Card: Spend in local currencies abroad without hidden conversion markups

- Batch Payments & API: Pay many international contractors at once, with an API for automation

Pricing

| Plan | Monthly | Annual (per month) |

|---|---|---|

| Wise Business | $0 | $0 (one-time setup fee; per-transfer FX fees) |

Pros

- Cheapest, most transparent FX in the category

- Local account details across dozens of currencies

- Excellent for paying overseas contractors and collecting globally

- Batch payments and API for automation

Cons

- Not a full bank — no lending or US treasury

- US balances safeguarded/pass-through, not directly FDIC-insured

- Best as a complement to a primary operating account

Verdict: Wise Business is the international pick. If your startup pays or collects across borders, hold it alongside your main account — the FX savings alone typically pay for themselves within the first few transfers.

Visit Wise BusinessHow to Choose the Best Business Bank Account for Your Startup

The decision framework, by the situation that actually decides it:

If you just raised a venture round

Protect the runway first: you want expanded FDIC coverage and yield on idle cash. Mercury is the default — a clean operating account with sweep-based coverage and treasury built in. Arc adds venture debt for non-dilutive runway extension, and Rho consolidates cards and AP alongside banking. For managing the raise itself, see our guide to the best treasury & cash management software.

If you're a bootstrapped small business

You run on operating cash, so control and organization matter more than treasury. Relay gives you up to 20 accounts for Profit First or envelope allocation and deep QuickBooks/Xero sync; North One bakes envelope budgeting into a single account; Bluevine earns APY on your checking balance and offers a line of credit when you need capital.

If you're a solo founder or freelancer

You're also your own bookkeeper and tax department, so pick an account that helps with both. Found is close to ideal — free checking with automatic tax estimates and built-in bookkeeping for sole proprietors; Novo is the simplest free account with invoicing and small-business integrations. Both open in minutes with no minimums.

If middleware risk worries you

If the fintech-over-partner-bank model gives you pause after the Synapse episode, go straight to a charter. Grasshopper is a real chartered digital bank — your deposits are held directly by an FDIC-insured institution, with a modern app, interest-bearing checking, and access to lending and SBA products. Many teams also keep a portion of reserves in a brokerage or a traditional bank as a second counterparty.

If you operate across borders

Paying overseas contractors or collecting from foreign customers is where traditional banks quietly overcharge on FX. Wise Business gives you local account details in dozens of currencies and converts at the mid-market rate — hold it alongside your primary account rather than as a replacement. Mercury and Rho also support international wires if you'd rather keep one platform.

Pro Tip

Open your primary account before you need it — most platforms want your EIN and formation documents, and onboarding can take a few days if the partner bank flags anything. And don't over-consolidate: keeping a second account at a different institution (or a chartered bank) means a single provider outage or freeze never locks you out of payroll.

Frequently Asked Questions

Final Thoughts

The best business banking for your startup depends on one distinction and two facts: whether you want a fintech platform or a chartered bank, how much cash you hold, and how you spend and move it. Mercury is our best-overall pick because it combines the cleanest software with sweep-expanded FDIC coverage and treasury — the safe default for most startups — but Relay is the right answer for bookkeeper-led cash management, Arc for venture-backed runway, Found for solopreneurs, Grasshopper for founders who want a real charter, and Wise Business for anything cross-border — and each would be right for the team it fits.

Whatever you pick: confirm which FDIC-member bank holds your deposits and how far coverage extends, read the transaction fee schedule rather than the “no monthly fee” headline, and consider keeping a second account at a different institution so no single freeze can lock you out of payroll. Get the plumbing right early and business banking becomes invisible infrastructure — exactly what you want it to be.

Related Free SEO Tools

Content Brief Generator

Generate SERP-grounded briefs for your category content

SEO Content Grader

Score your comparison and alternative pages

Meta Tags Generator

Optimize SERP previews for landing pages

Long-Tail Keyword Generator

Find low-competition commercial queries

Keyword Search Volume

Size demand for your product category

SERP Checker

See who ranks for your target keywords today

Related Articles

Best Treasury & Cash Management Software

Put idle runway to work with yield and expanded coverage

Best Corporate Cards for Startups

The card programs that pair with startup banking platforms

Best Expense Management Tools

Automate receipts, spend controls, and the month-end close

Browse All Articles

Explore our complete library of guides and tutorials

About the Author

Co-Founder & SEO Execution

Co-founder of PikaSEO. 11 years in corporate tech, then bootstrapped entrepreneur. Leads SEO execution and content-led growth for SaaS companies.